Fundraising activity has reached its lowest level in the past three years. This can be attributed to the tightening monetary policy and the lack of new disruptive protocols. The limited variety of existing solutions has resulted in the emergence of numerous similar protocols. Consequently, the size of funding rounds has decreased as money has become more expensive and similar projects have proliferated.

For more insights and a detailed analysis of October’s investment trends, we invite you to read our new Crypto Fundraising Recap.

Executive Summary:

- Crypto fundraising is currently experiencing a downturn, but the recent price rally and the potential approval of a Bitcoin ETF could stimulate fundraising activity.

- The tightening monetary policy in the US has resulted in smaller round sizes and reduced overall investment.

- A total of 112 deals worth $430 million were closed.

- The highest funding amounts were received by Blockchain Service ($161.7M) and DeFi ($128.7M).

Fundraising Round Size Decreased, While the Number of Rounds Increased

The number of projects attracting investments continues to rise, with 112 projects raising investments in October, compared to 99 in September and 63 in August. However, in terms of funding, there was a decrease compared to the previous month, with $430 million raised in October, down from $562 million in September, although still higher than the $349 million raised in August, two months prior.

In October, there was a notable surge in cryptocurrency prices towards the end of the month. The price of Bitcoin increased by 21%, breaking the psychologically important mark of $30,000. Altcoins followed Bitcoin’s upward trend. If the price of cryptocurrencies remains at the current level, there is reason to expect increased activity from both venture capital funds and new projects.

Alongside the price increase, the battle between layer-2 ecosystems for users and the expectation of Bitcoin halving in April 2024 may help revive investment in new projects. However, the global rise in the cost of money may limit this growth and even eliminate it.

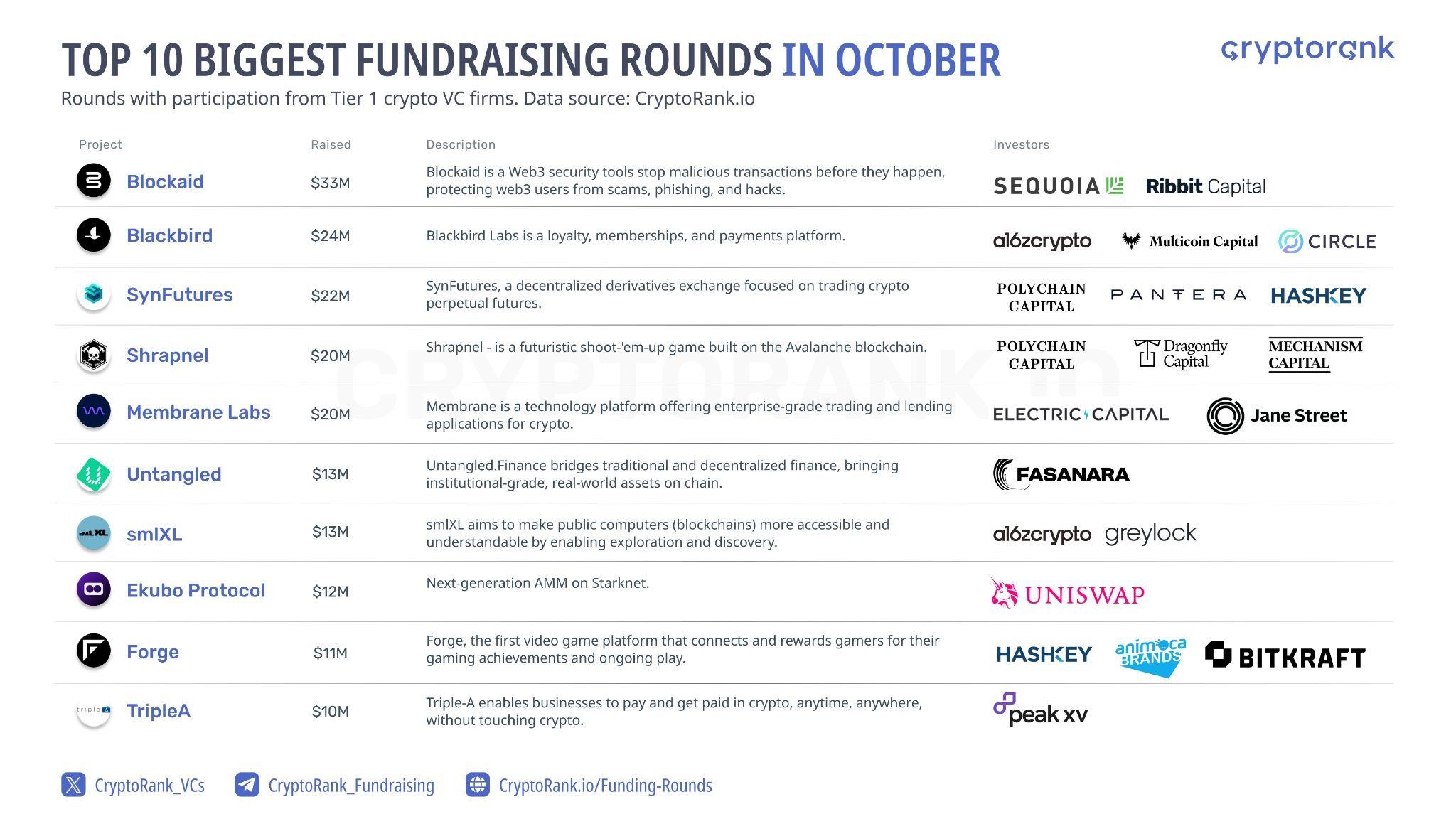

Monthly Focus: Biggest Funding Rounds

In October, the top 10 biggest rounds accumulated a total of $178 million, which accounted for 41% of all VC investment in that month.

Now, let’s take a closer look at the top 3 leaders:

- Israeli web3 security company Blockaid has emerged from stealth mode after raising a total of $33 million. The recently completed Series A financing round was led by Ribbit Capital and Variant, with participation from Cyberstarts, Sequoia Capital, and Greylock Partners. The new funds will be used to further develop products, expand the development team, and grow its customer base. In less than a year, Blockaid has already acquired numerous customers, including Metamask, Opensea, Rainbow, and Zerion, with more to be announced soon.

- Blackbird Labs is an app and loyalty program that aims to connect restaurants and their customers through its crypto-powered app. The company recently announced that it raised $24 million in a series A funding round led by venture capital firm Andreessen Horowitz (a16z). Using Blackbird, which is built on Coinbase’s Layer-2 Base blockchain, customers can tap their phone on a near field communication (NFC) reader to create a non-fungible token (NFT) membership. The NFT is minted when users “tap in” to the restaurant.

- SynFutures is a decentralized derivatives exchange that specializes in crypto perpetual futures trading. The company recently secured $22 million in a Series B funding round led by Pantera Capital, with participation from HashKey Capital, SIG DT Investments, and others. Alongside the funding announcement, SynFutures is unveiling its enhanced exchange, featuring the innovative “Oyster automated market maker”. SynFutures’ vision is to combine orderbook and AMM models, ultimately improving trading efficiency by consolidating liquidity within the DeFi space.

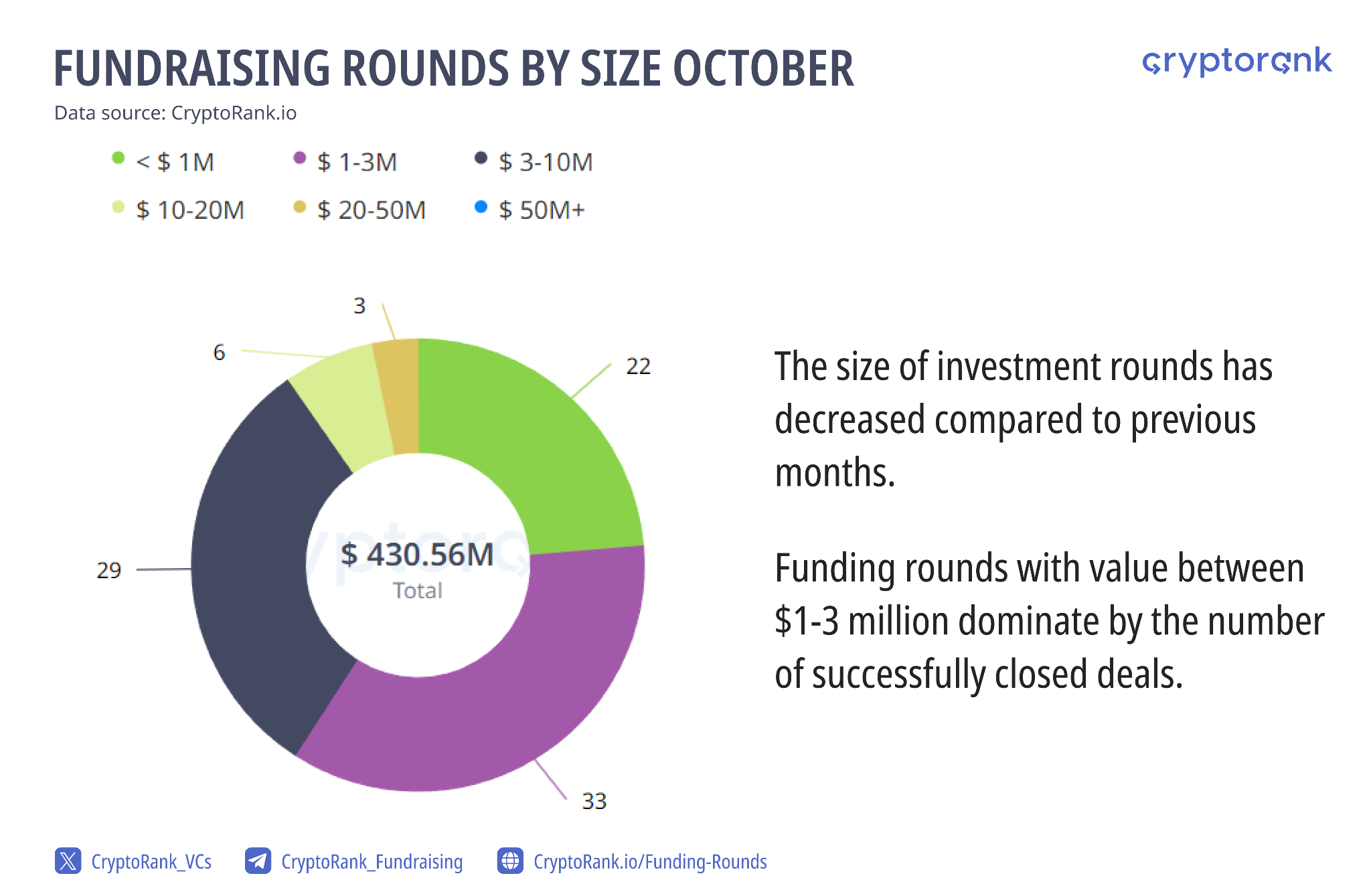

Fundraising Rounds by Size in October

In October, venture capital showed reluctance to make significant investments in the crypto market. Only 9 rounds exceeded $10 million, indicating a cautious approach. This suggests that venture capital does not anticipate significant industry growth in the near future.

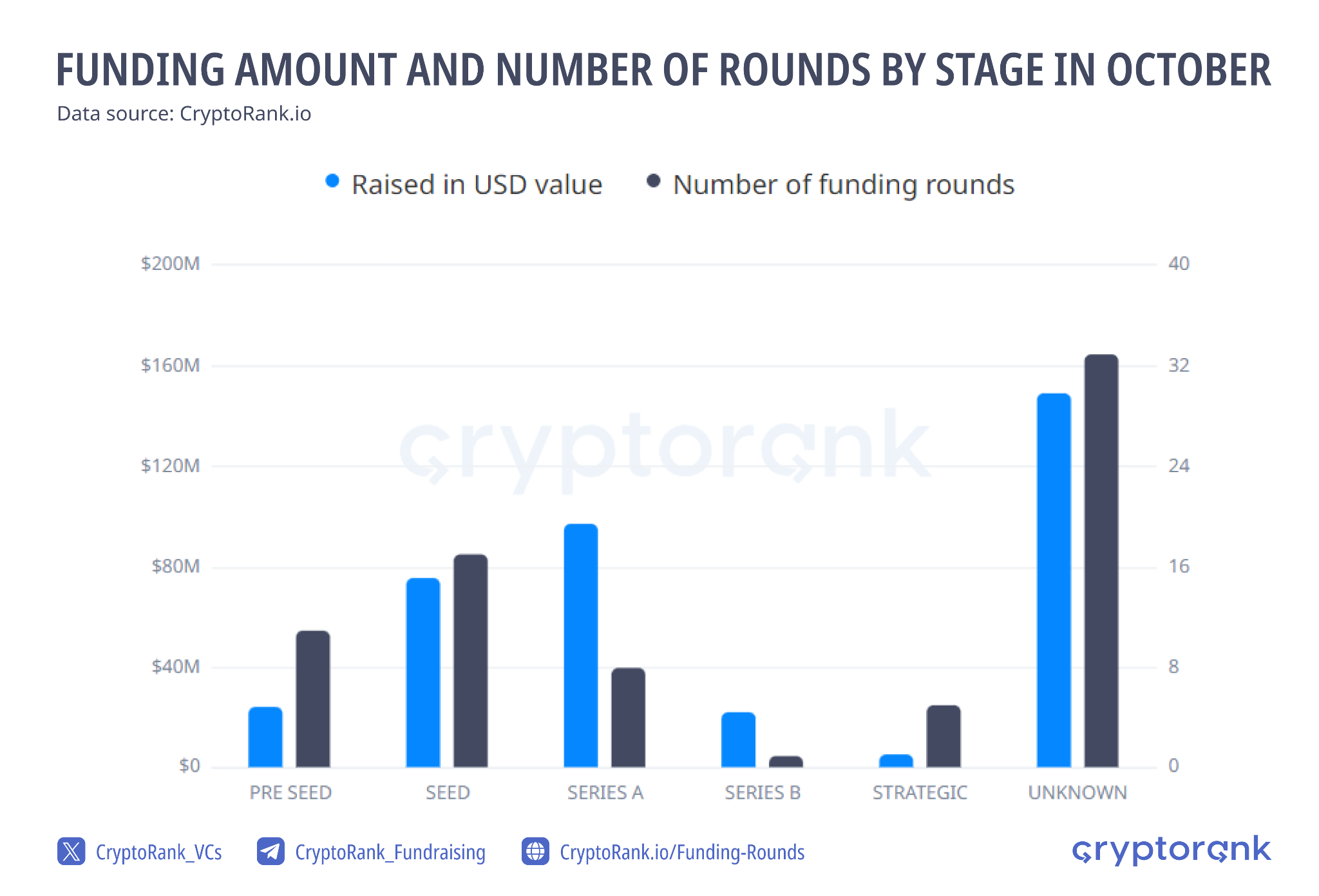

Funding Amount and Number of Rounds by Stage in October

The chart below demonstrates that venture capital largely prioritizes early-stage investments, with a particular focus on emerging projects. Although there are a significant number of undisclosed deals, there is no indication that the distribution would change if these deals were made public.

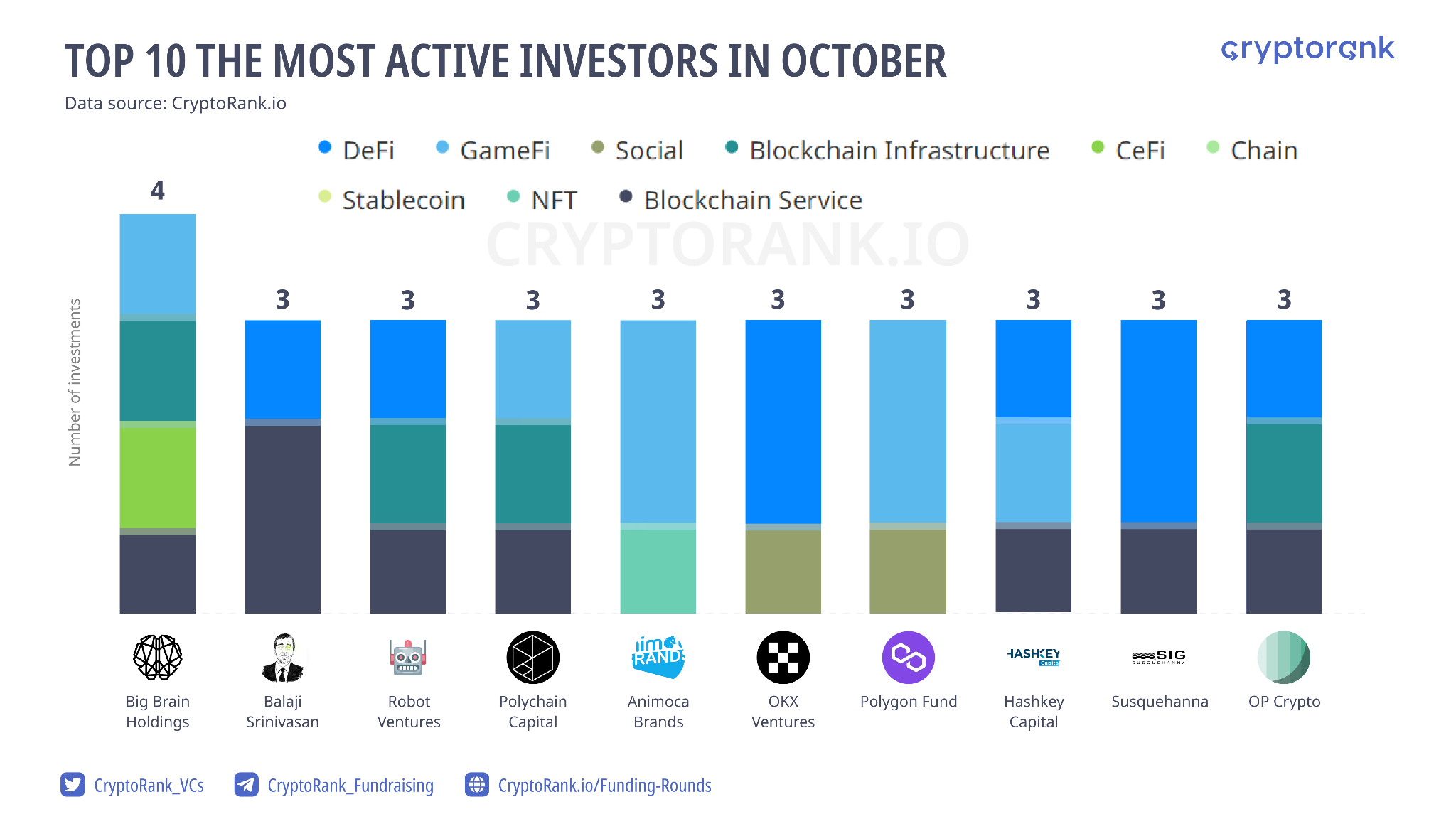

Most Active Funds in October

Out of the 112 investment rounds in October, the top ten most active investors accounted for 31 deals, which is approximately 26% of all rounds.

Andreessen Horowitz (a16z) is reportedly preparing to raise $3.4 billion for its upcoming early and seed-stage venture funds. As the largest venture capital firm in terms of assets under management, it plans to launch its fundraising campaign by the end of this year and aims to conclude it in the first half of 2024. This is a positive sign for the industry as a whole.

Trending Categories in October

In October, DeFi emerged as the most popular category in terms of funding rounds, with 41 rounds. It was followed by Blockchain Services with 36 rounds, and GameFi with 10 rounds. However, in terms of the amount of money raised, the Blockchain Service category took the lead, securing $161.7 million last month. Startups in the DeFi and GameFi sectors raised $128.7 million and $53.3 million, respectively.

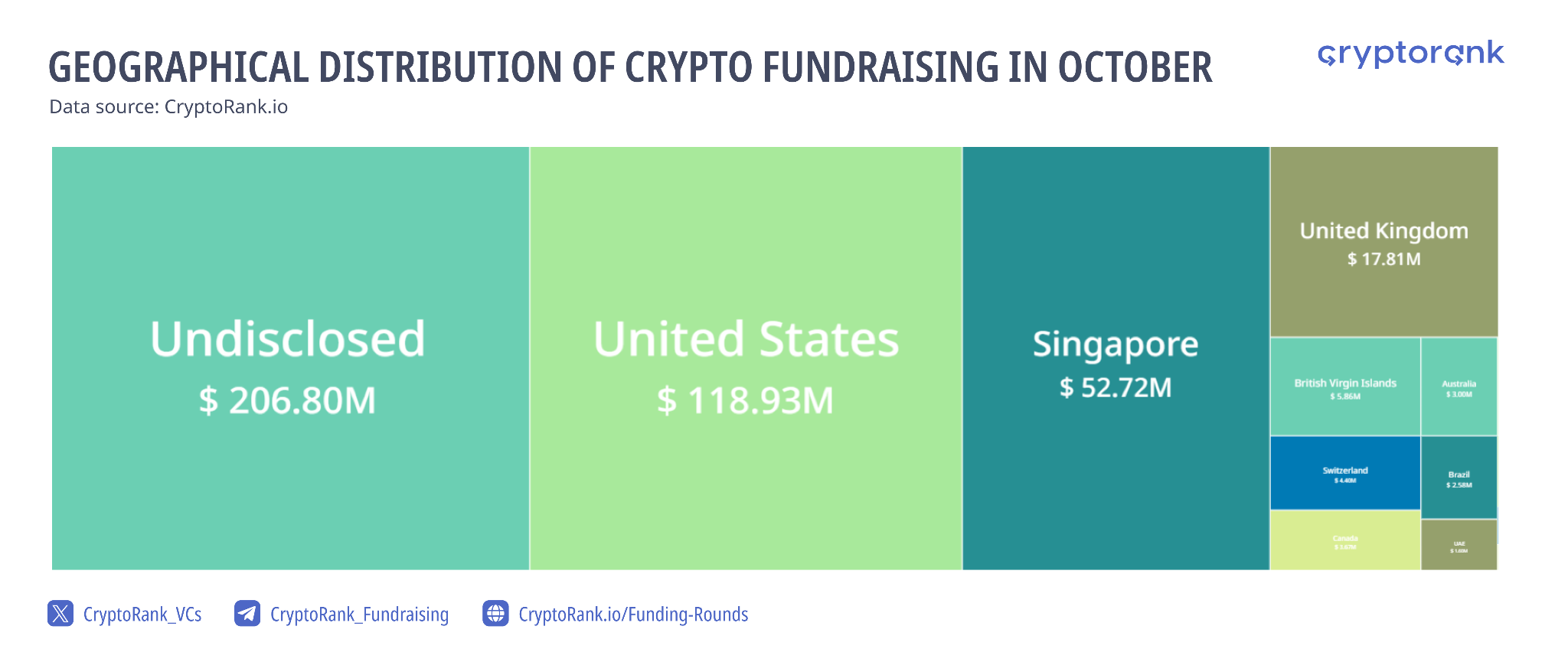

Geographical Distribution of Fundraising Activity in October

The United States continues to be the leading venture hub in the industry, with a total investment of $118.9 million spread across 24 rounds. Singapore secured the second spot in October, investing $52.7 million across 12 rounds in terms of both funds and deals closed. It is worth noting that 52 rounds, accumulating a total of $206.8 million, remained undisclosed, accounting for approximately half of the investment rounds in October.

The Bottom Line

A slight increase in fundraising activity may be supported by the recent price rally and the upcoming Bitcoin halving, which could potentially lead to heightened fundraising efforts during the winter months. November will be a crucial month for assessing the fundraising landscape. If both fundraising and cryptocurrency prices continue to rise, it could indicate the start of an upward trend. On the other hand, if November ends with lower fundraising activity and price levels compared to October, it may suggest a period of continued stagnation.

Disclaimer: The information presented in this article is for informational and educational purposes only. The article does not constitute financial advice or advice of any kind. Coin Edition is not responsible for any losses incurred as a result of the utilization of content, products, or services mentioned. Readers are advised to exercise caution before taking any action related to the company.