The latest KuCoin Ventures Weekly Report highlights an important shift in institutional behavior between June 22 and 28. On the surface, market conditions offered little reason for optimism. Tightening financial conditions, sticky inflation, a hawkish Fed, and a seventh straight week of Bitcoin ETF outflows should have sent institutional capital for the exits. However, institutional positioning suggested otherwise. Instead, the week’s developments pointed to a different trend. Investors became far more selective, moving toward sectors with real yield, real fundamentals, and real utility rather than fleeing altogether.

Three areas absorbed most of that attention: real-world assets (RWAs), DeFi lending, and prediction markets. Aave deepened its footprint in institutional on-chain lending, Kraken emerged as a possible buyer into that same infrastructure, and prediction markets kept pulling in capital even as broader crypto fundraising slowed. Taken individually, none of these is a huge story. Together, they point to the same thing: liquidity rotating toward blockchain infrastructure built for actual financial activity, not speculation.

The Fed Sets the Tone

Geopolitical risk between the U.S. and Iran eased somewhat during the week, but that barely registered next to the market’s real concern: what the Federal Reserve would do next.

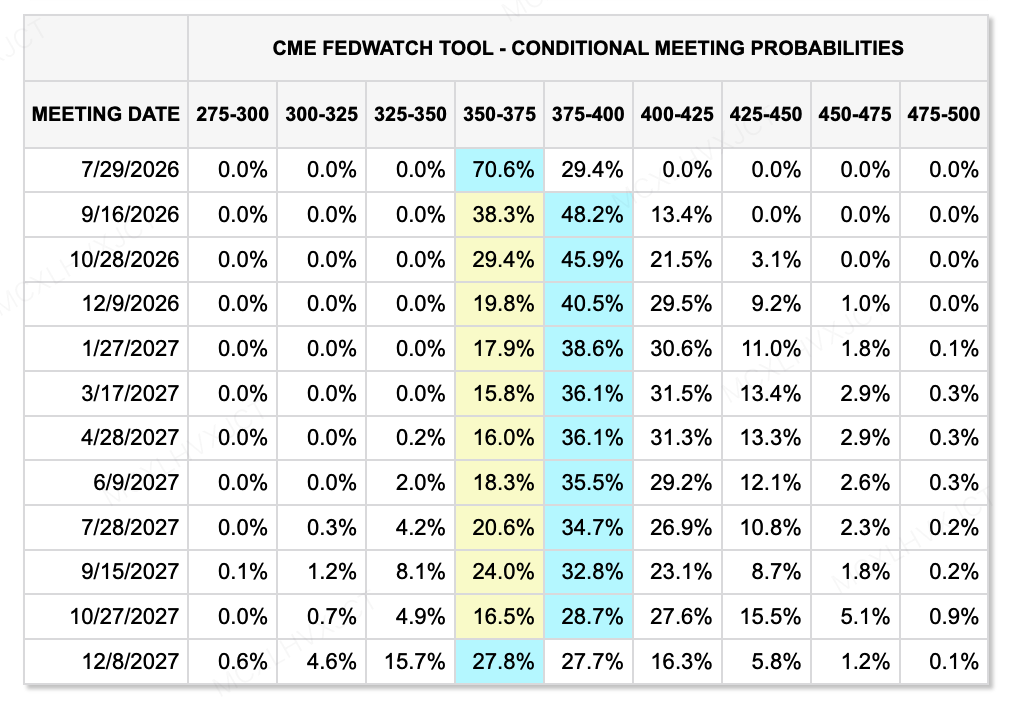

At his first FOMC meeting as Chairman, Kevin Warsh held rates steady at 3.50%–3.75%, but stripped out the forward guidance entirely, pushing the Fed toward a fully data-dependent posture. Policymakers also nudged their inflation forecast up to 3.6%. Put those two things together, and the message is simple: don’t expect cuts anytime soon. The CME FedWatch Tool backed that up, with markets pricing in elevated rates across upcoming meetings rather than any near-term easing.

Equities felt it immediately. The S&P 500 dropped nearly 2%, and the Nasdaq 100 fell more than 4% as investors dumped high-growth tech, AI names especially. Leveraged ETFs made the swings worse; their rebalancing mechanics amplify moves in both directions, and with over $270 billion in global AUM sitting in these products, that amplification effect is no longer a footnote; it’s a structural feature of how volatility spreads through markets now.

Bank of America added to the hawkish mood, forecasting three rate hikes starting in September for a combined 75 basis points. Yet the bank didn’t turn bearish on growth; it actually raised its global GDP forecasts to 3.2% for 2026 and 3.5% for 2027.

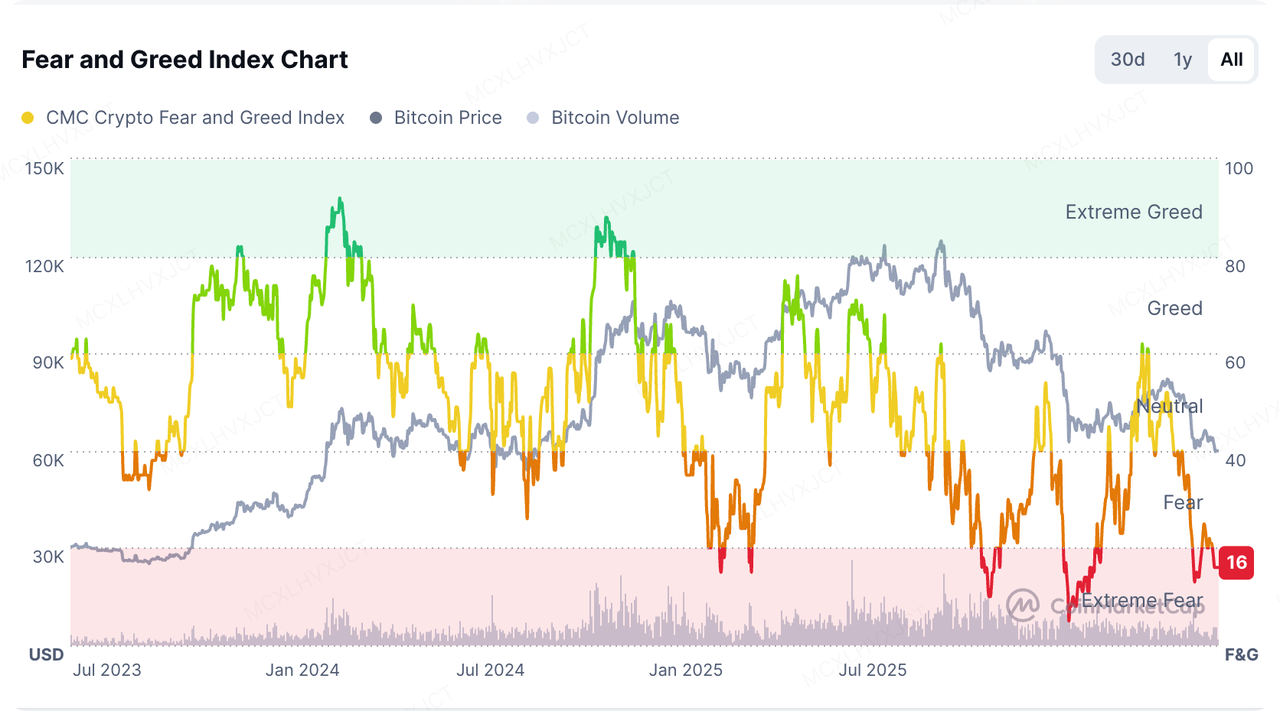

Crypto absorbed the same pressure. U.S. spot Bitcoin ETFs saw roughly $1.79 billion in net outflows, the second-highest weekly figure on record and the seventh consecutive weekly outflow, bringing the 20-day cumulative total to about $5.42 billion, the worst stretch on record. BlackRock’s IBIT bore the brunt of it, logging its own seventh straight week of outflows with a single-week redemption of $860 million. Meanwhile, the Crypto Fear & Greed Index dropped to 15, into Extreme Fear, as leveraged and speculative positions got unwound.

None of this looks like capitulation, though. It looks like repositioning. Investors weren’t leaving crypto; they were deciding where in crypto to be.

The Macro Picture Beyond the Fed

Tensions between the U.S. and Iran eased over the week, with both sides agreeing to halt attacks and plans to resume talks in Qatar focused on the Strait of Hormuz. The U.S. Treasury backed that de-escalation with General License X, permitting Iranian oil sales to be settled in dollars. Brent crude gave back its risk premium accordingly, drifting down to around $72.50 a barrel.

That combination, easing geopolitical risk and tightening monetary risk, showed up clearly in currency markets. The dollar index pushed higher, and non-dollar currencies took the hit: USD/JPY held above 160, the pound came under pressure even after the Bank of England voted 7-2 to hold rates at 3.75%, and the People’s Bank of China ran its first-ever 300 billion yuan overnight reverse repo to smooth out quarter-end liquidity strain. Inflation data didn’t help the Fed’s case for patience either. Richmond Fed President Tom Barkin flagged May’s PCE print at 4.1% year-over-year, the highest since April 2023, with continued AI infrastructure buildout cited as one factor keeping price pressure sticky.

The unwind on the equity side was messier than the headline index numbers suggest. Much of the damage in AI-linked names came from retail-driven selling colliding with leveraged ETF mechanics, a reminder that products designed to amplify returns amplify losses just as efficiently. One leveraged fund tied to SpaceX dropped roughly 40% almost immediately after listing, catching investors who bought near the top. Strategy Inc.’s crypto-leverage ecosystem told a similar story: its long-short leveraged ETF, launched in 2024, is now down more than 90% since inception, and its preferred stock (STRC) fell below $71 against a $100 target price, a sign that forced deleveraging, not just sentiment, was driving part of the move.

It’s worth separating that from a genuine liquidity crisis, though. Unlike the 2018 and 2022 selloffs, which were driven by outright Fed tightening and M2 contraction, the broader liquidity pool, Fed balance sheet size, and M2 growth kept expanding through this period. That distinction matters: what markets went through reads more like profit-taking and leverage clearing after a long AI-driven run than the start of a systemic liquidity squeeze.

RWAs Move Beyond Tokenization

The RWA conversation has quietly changed. A year or two ago, the goal was simple: get a Treasury bill or a money market fund onto a blockchain and call it done. Now the question is different: Can that tokenized asset actually do something once it’s there? Can it be pledged, borrowed against, or refinanced?

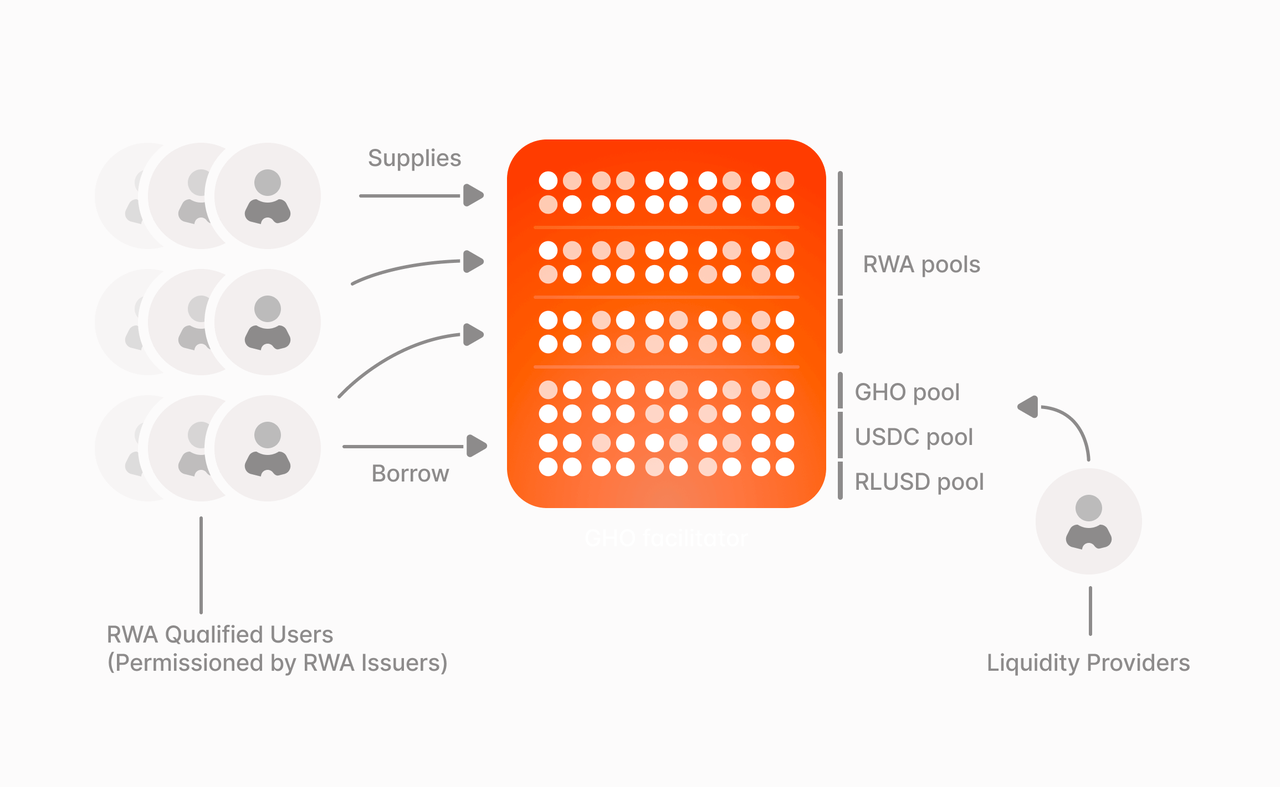

Aave Horizon is the clearest test case for that shift. It’s a bridge: a permissioned collateral layer lets qualified institutions post tokenized Treasury bills and funds as collateral, while a permissionless liquidity layer lets anyone supply stablecoins, USDC, RLUSD, GHO, to fund that borrowing. The result is that previously inert tokenized assets become working collateral inside an actual credit market.

According to available data, Horizon has reportedly pulled in hundreds of millions in deposits and is generating real borrowing demand, not just idle liquidity. That’s the detail that matters here; it means tokenized assets are starting to circulate rather than just sit. If that keeps up, RWA success won’t be measured by how much value gets tokenized, but by how much of it actually moves through on-chain credit markets.

Aave’s Growing Institutional Role

Aave’s growing role in this shift has also attracted institutional attention. Standard Chartered’s Global Head of Digital Asset Research, Geoff Kendrick, initiated coverage on AAVE with a long-term price target of $3,500 by the end of 2030, arguing that growth in tokenized RWAs should drive more borrowing activity toward established DeFi lenders. Notably, the report doesn’t treat AAVE like a speculative token; it treats it like infrastructure that stands to benefit as traditional finance tokenizes more of itself, increasingly evaluated on deposits, lending volume, net interest margins, and protocol revenue rather than crypto-native leverage cycles.

If that thesis holds, Aave’s trajectory stops being about crypto market cycles and starts being about institutional adoption speed. Mature liquidity and proven risk management matter more to a bank evaluating on-chain lending than they do to a retail trader chasing a cycle, and that’s exactly the audience Aave increasingly seems to be building for.

Kraken Expands Its RWA Strategy

Kraken moved in a similar direction, although its strategy unfolded differently. The exchange had already completed its acquisition of Backed Finance, a firm that specializes in bringing regulated financial assets on-chain, including tokenized equities and exchange-traded products. The acquisition aligns with the broader trend toward tokenized real-world assets, just applied to a different asset class. Where Horizon is building the credit rails for tokenized Treasuries and funds, Backed Finance gives Kraken the issuance and settlement infrastructure for tokenized equities, folded further in-house under its xStocks product. Two different pieces of the same thesis: real-world assets only matter once they’re wired into something that can trade, settle, or lend against them.

That strategy appeared to extend even further during the week. Kraken’s parent company, Payward, was reportedly in talks to acquire roughly 15% of Aave Group at a valuation of around $385 million. Aave’s founders pushed back on parts of the report, including the claim that AAVE was being sold at a steep discount, and the deal remains unconfirmed. Denied or not, the rumor fits the pattern: an exchange that already owns RWA-issuance infrastructure exploring a direct stake in RWA-lending infrastructure. If it happens, Kraken wouldn’t just be adjacent to the RWA story; it would own meaningful pieces on both sides of it, tokenization and credit.

Look at Aave and Kraken side by side, and a pattern emerges. Lending protocols are absorbing institutional RWA collateral and stablecoin liquidity. Exchanges are pushing outward from pure trading venues toward multi-asset financial gateways, tokenized equities, yield products, and now potential direct stakes in the protocols underneath it all. Different starting points, same direction of travel.

Prediction Markets Buck the Funding Slowdown

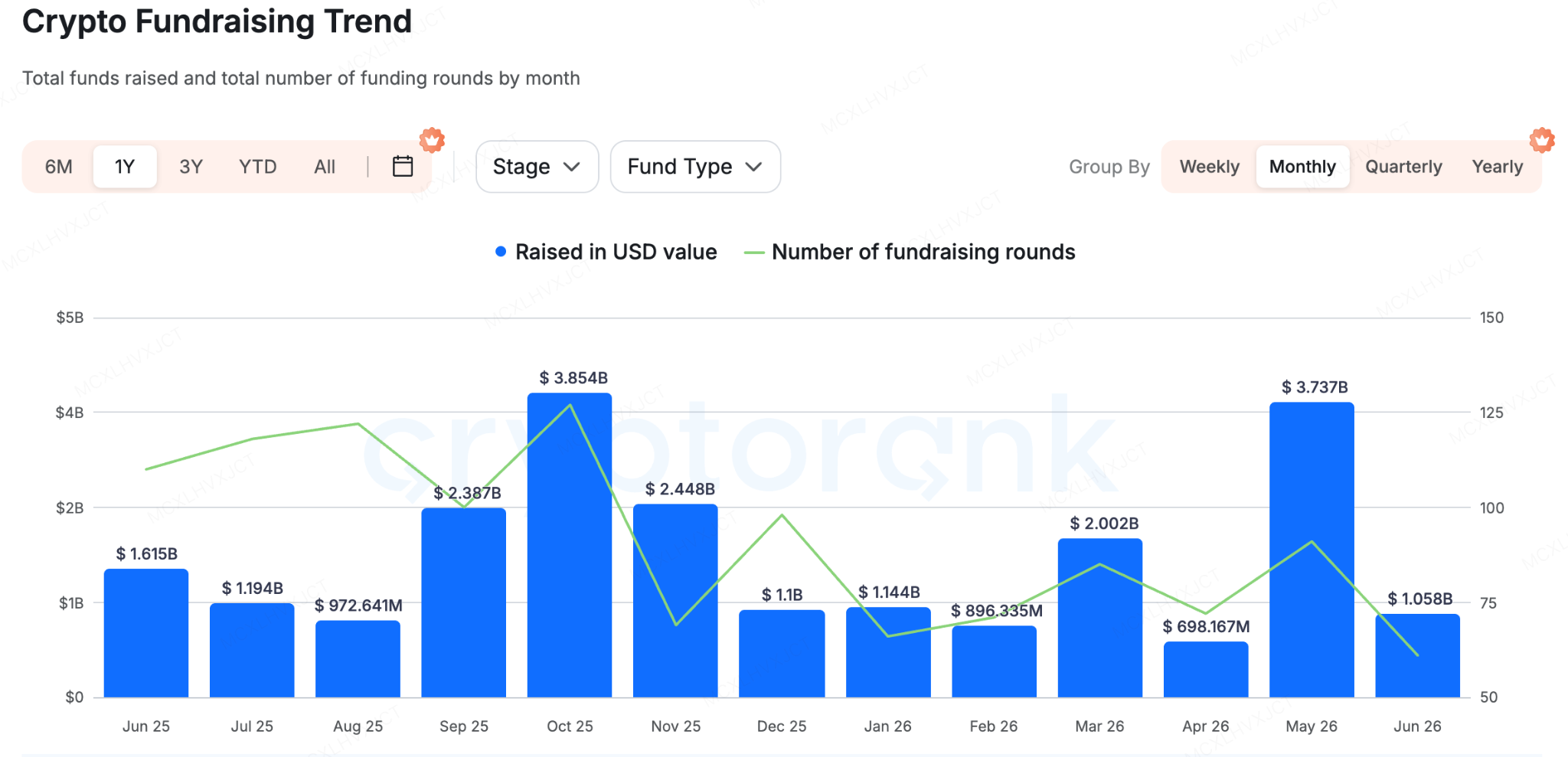

Crypto fundraising overall had a rough June; industry-wide funding fell from $3.737 billion in May to $1.058 billion in June. That’s not a sector collapsing so much as investors getting pickier about where dollars go, and consolidation activity picked up alongside it: crypto platform Bitbank agreed to a $289 million acquisition deal on June 25, and Suilend and 250 Digital both closed mergers in the same stretch. Capital that stayed active concentrated hard on infrastructure, AI-adjacent plays, and a handful of specific applications, prediction markets chief among them.

The standout deal: Onyx Odds closed a $20 million Series A led by Payward Inc., Kraken’s parent company, pushing the company’s valuation to $220 million. Onyx started in 2025 as a free social sports prediction platform running in more than 40 U.S. states, using a dual virtual-currency model to stay compliant where real-money sports betting isn’t allowed. It has since moved steadily toward becoming a regulated prediction market operator.

That pivot picked up speed after Onyx struck an exclusive partnership with Polymarket in November 2025, giving it a path to launch CFTC-regulated sports event contracts. Payward’s investment adds real regulatory muscle to that plan. Payward holds both Futures Commission Merchant and Designated Contract Market licenses from the CFTC, which could meaningfully shorten Onyx’s road to market. The partnership is also expected to fold crypto trading directly into Onyx’s platform, tying prediction markets and digital assets closer together.

The broader implication is that investors aren’t treating prediction markets as a novelty betting product anymore. They’re starting to look like regulated financial infrastructure that happens to combine forecasting, trading, and crypto in one place, and in a funding environment this selective, that kind of backing says something about where the sector is headed.

Where This Leaves the Market

The week’s developments point more toward selective capital allocation than broad risk aversion. Higher rates and macro uncertainty kept sentiment cautious all week, but institutional capital didn’t pull back; it redirected toward sectors with fundamentals that hold up regardless of the rate cycle. RWAs, DeFi lending, tokenized finance, and prediction markets all point in the same direction: crypto’s center of gravity is shifting from speculative upside toward infrastructure that does real financial work. That’s a slower story than a bull run, but it’s arguably a more durable one.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources. As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer

This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn’t guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.

Disclaimer: The information presented in this article is for informational and educational purposes only. The article does not constitute financial advice or advice of any kind. Coin Edition is not responsible for any losses incurred as a result of the utilization of content, products, or services mentioned. Readers are advised to exercise caution before taking any action related to the company.

Price Prediction 2026, 2027, 2028, 2029, 2030-2050")