As the development of crypto transactions moves beyond exchanges and wallets, crypto payment cards are becoming a viable option that allows spending digital currencies in real-world purchases. Whether you are buying coffee, paying for online goods, withdrawing cash from the ATM, or making a payment with your Apple or Google Pay, crypto payment cards make the link between cryptocurrencies and regular financial networks.

While many crypto payment cards do not allow spending highly volatile cryptocurrencies directly, some companies have opted for stablecoin transactions or crypto-based loans rather than spending the digital currencies directly. Each service uses its own approach, either transferring digital currencies instantly at the moment of transaction or lending users money based on their crypto wallet balance.

Let’s check out five popular crypto payment card services in 2026.

Top 5 Crypto Card providers of 2026

Not all cryptocards are made equal, and currently, all major card providers focus on stablecoins rather than allowing you to pay with PEPE for a meal; still, they are good tools.

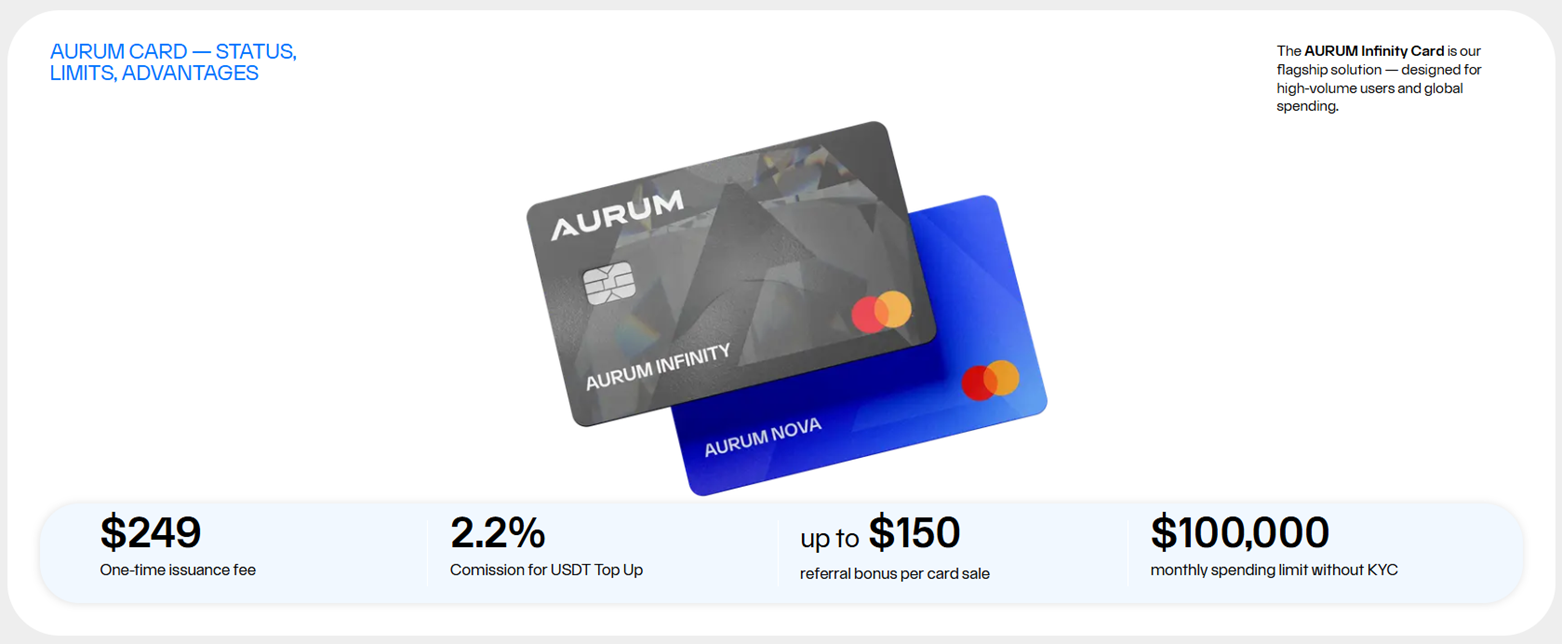

Aurum Neobank Card — The USDT Go-to Solution

Aurum Foundation offers a simple USDT stablecoin card with 3 distinct features: Cards can be topped up with USDT, and used to pay for goods or services without additional conversion steps via Apple Pay or Google Pay like a normal card; Card is designed to function globally, and work with global ATMs and Point-of-Sale machines, as well, as to withdraw cash on demand; KYC-Free Spending — Aurum Foundation promises a spending tool that doesn’t ask to flash your ID.

Aurum Card doesn’t need intermediate steps, like usual back-and-forth swaps between card and exchange, then to the bank account, and so on. Exchange happens directly and instantly, at the point of sale, right after you flash the card.

The card is controlled via an app and integrated into the Aurum Ecosystem. By using the Aurum Neobank app, users can control their USDT balances, view transaction history, monitor AI yields, and manage card security (freezing and unfreezing it on demand).

Issuing terms are reasonable: $249 one-time issuance fee, 2.2% top-up commission, up to $150 referral bonus per card sale, and up to $100,000 monthly spending limit without KYC. To power the card with a dedicated hardware wallet, Aurum Foundation partnered with Tangem to release 1000+ co-branded wallets.

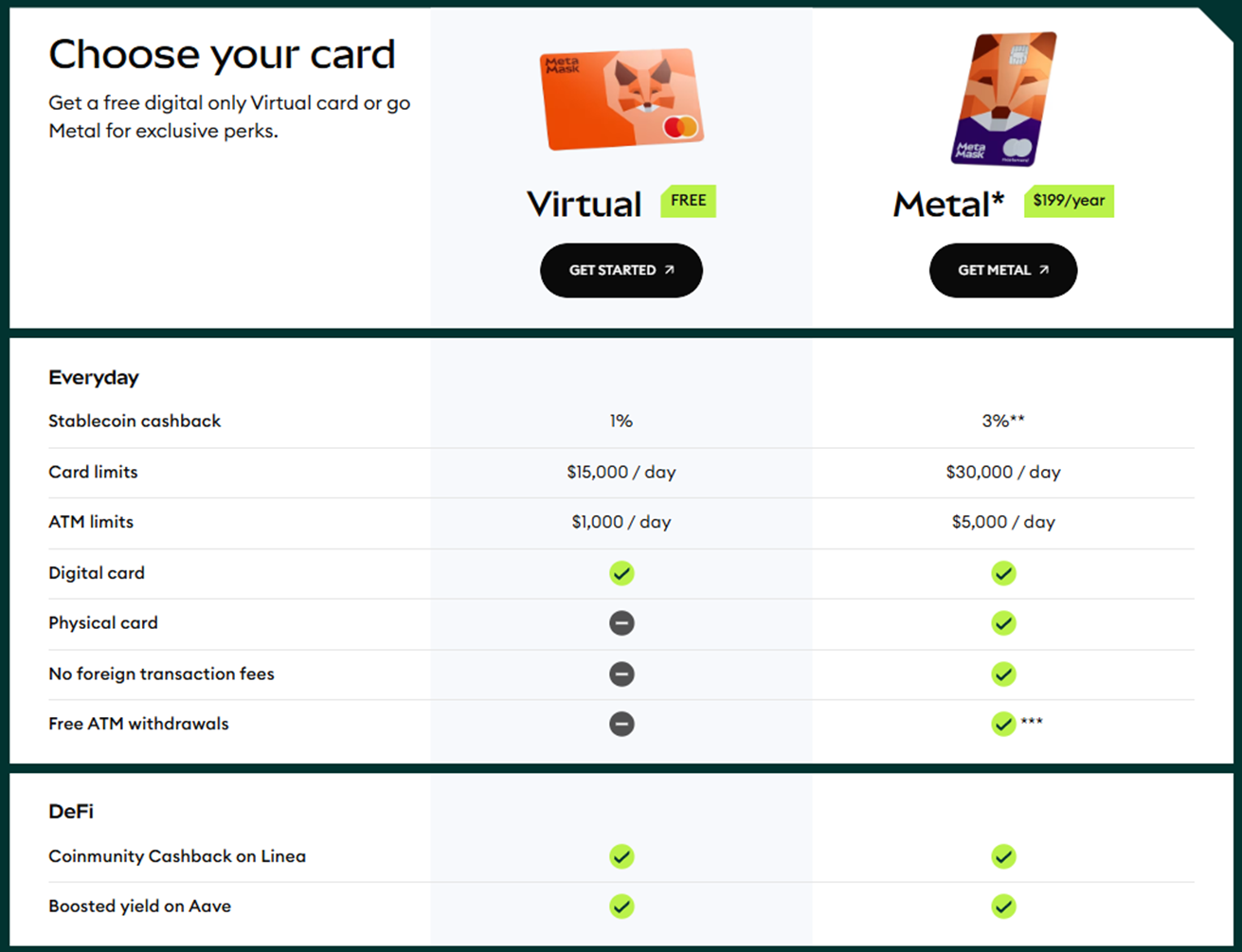

MetaMask Card — On-Chain Spending with Some Limitations

The asterisk in the headline doesn’t immediately cross it out as bad. Metamask card is quite good and offers spending directly from the Ethereum wallets via the EOA system. It also allows the use of stablecoins such as mUSD, USDC, or wETH.

What does the asterisk actually say? Well, in order for the card to work,k users have to wait a few moments to minutes for the card to actually convert crypto via dedicated networks on currently supported L2 chains, and as of 20,26 those are primarily Linea and Base, along with paying a network fee for this instant transaction.

There is no true global access. MetaMask card is good in the UK, EU, and LATAM (until new regulations are imposed), and US users can even try to have one, but it requires KYC verification.

Liquidity Management is on the user: to use cards properly, one has to make sure they are allocated funds to the proper network, such as Linea or Base. Solana spending via MetaMask card has faced state-by-state restrictions in the US.

Card terms are good: 1% cashback for virtual card, 3% for metal one, free ATM withdrawals of up to $1,200 with 2% after that.

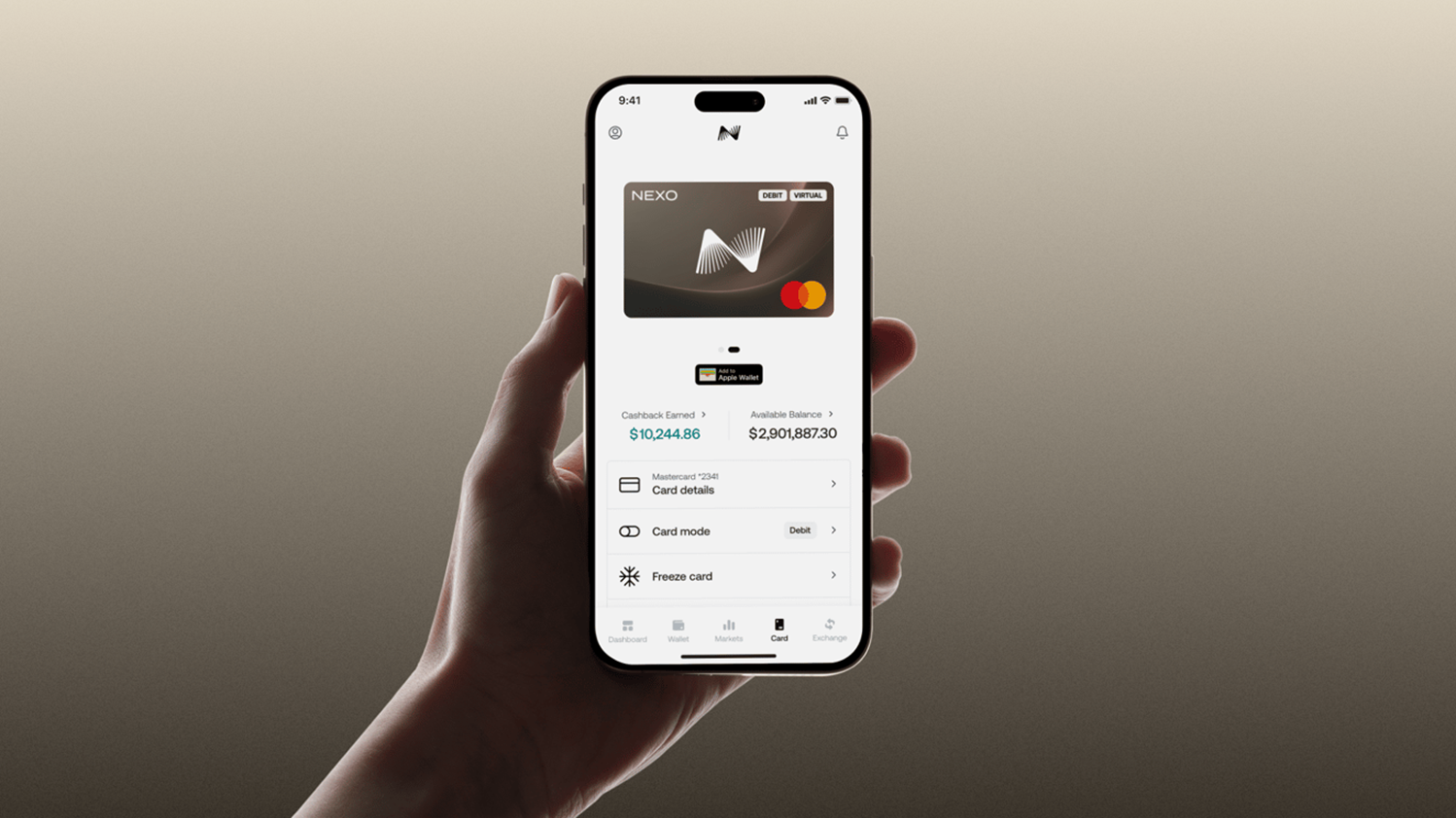

Nexo Card — Unlocking Crypto Liquidity

The Nexo card team found the most legal loophole: in some jurisdictions, selling crypto is a taxable event, but using it as collateral for a loan is not. That is the whole premise of Nexo — use crypto you already own to power flash loans at the point of sale.

The Nexo card is designed to be a crypto credit card, rather than a debit one. The amount of capital available for spending is defined by the loan-to-value ratio, which depends on the volatility of the asset. For instance, with Bitcoin, it’s 50%, which would mean that out of a $10,000 BTC collateral car,d one can use $5,000 in fiat for spending.

On the plus side, it’s a legally allowed loophole, which has been known since the 1980s: corporation CEOs could use their own stock as collateral for a bank loan, which is then used for operational expenses depending on local tax regulations. This is not a bug, but a feature of a financial system.

The whole purpose of Nexo is not to be a crypto card for spending, but rather to help people who want to unlock part of their own liquidity in crypto for everyday expenses without the need to pay taxes.

To compensate for actually taking a loan, Nexo offers 13% APY on the balance paid out daily, access to anywhere a Mastercard is accepted, no inactivity or credit card fees, and integration with Google and Apple Pay systems.

RedotPay Card — for spending BIG every day

RedotPay Card offers the same approach as Nexo, using crypto as collateral to avoid taxes, with a built-in P2P market to exchange crypto-to-fiat and vice-versa from local merchants. It supports USDT, USDC, BTC, ETH, and SOL, and offers real-time conversion to fiat at the point of sale.

Pay in fiat loans, avoid taxes for selling crypto, and use your portfolio as collateral. Higher spending limits are available: $ 1M per single transaction and up to $1M daily, provided users complete KYC.

Fees are “variable”: for merchants like Discord, Facebook Ads, or PUBG Mobile, it can be 1.5% with a minimum of 50 cents, 2% for ATM withdrawals for up to $10k in cash, and 3% above that. It may not sound like an issue, but you’d be paying $300+ from each $10k+ withdrawal.

Geolocks are present: RedotPay is operated by a centralized entity, and blocks users from major Sanctioned Regions, China, Russia, and Ukraine. It is subject to standard KYC/AML laws and requires standard KYC verification for the end user.

MEXC Crypto Card — for spending the trading capital on hookah n’ snacks

MEXC offers a direct off-ramp for traders as a crypto card tied to a balance on the exchange. Instead of withdrawing funds from the exchange to a bank account and going through the friction of P2P trading, traders can just swipe their card at a cash register and use hard-earned profits to buy treats, pay for travel, or cover the cost of a hangover.

An MEXC card is handy for those who actively trade, and it works as a way to use trading profits without the need to withdraw them to a banking account. It’s a good option when one would like to use a portion of their holdings for momentary spending. On the downside, it uses the entire portfolio as a source of liquidity.

Disclaimer: The information presented in this article is for informational and educational purposes only. The article does not constitute financial advice or advice of any kind. Coin Edition is not responsible for any losses incurred as a result of the utilization of content, products, or services mentioned. Readers are advised to exercise caution before taking any action related to the company.

, Ethereum (ETH), XRP (XRP)")

, Shiba Inu (SHIB), MemeCore (M)")