- The XRPL Lending Protocol pairs a Single Asset Vault with onchain credit checks.

- Underwriting stays off-chain with institutions while protocol enforces the terms.

- The design avoids flaws seen in Aave, Compound, Maple, and Clearpool risk models.

Tokenization has solved one problem in blockchain finance: getting real-world assets like treasuries and money market funds onto a blockchain. But once those assets are onchain, a harder question remains. How do they actually become useful, rather than just sitting there?

That is the gap the new XRPL Lending Protocol is built to close.

Two Pieces Working Together

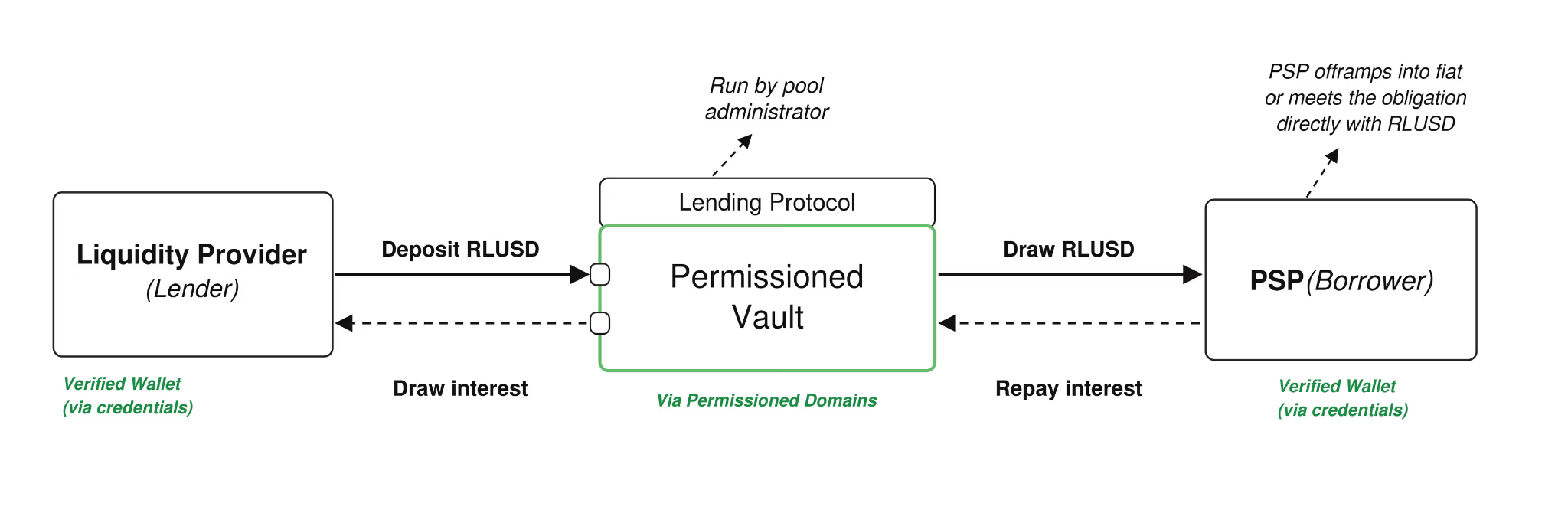

The system is built on two components. A Single Asset Vault pools and manages liquidity for a single asset onchain. The Lending Protocol then takes that pooled liquidity and originates it into loans with defined terms, servicing, and repayment logic. Together, they separate where liquidity is stored from how it gets put to work, mirroring how traditional capital markets keep custody and financing as distinct systems. These components are defined under XLS-65 and XLS-66, and remain subject to validator approval.

A Real-World Example

Consider a payment provider holding RLUSD reserves onchain, waiting on a cross-border settlement that will not close for another 48 hours. Rather than tapping an expensive bank credit line or selling assets at the wrong moment, the provider can borrow against expected settlement inflows through a licensed pool administrator.

Terms are agreed upfront, repayment is enforced automatically by the protocol, and there is no manual process or governance vote required at maturity.

The Key Design Choice

The protocol’s central principle is a clean split between credit judgment and credit execution. Underwriting, meaning the actual decision of whether a borrower is creditworthy, stays off-chain with institutions that already have credit teams, legal frameworks, and regulatory obligations. Once those terms are agreed, the blockchain takes over and enforces the mechanics: repayment schedules, interest calculations, and default conditions all follow predefined rules.

This matters because many existing onchain lending platforms, including Aave, Compound, Maple, and Clearpool, built underwriting assumptions directly into their protocol logic. When those models change through governance votes, institutions lose the ability to reliably evaluate risk in advance, which is a fundamental problem for how credit underwriting actually works.

Why It Matters Beyond XRP

The protocol also structures risk rather than spreading it across everyone. Pool administrators or underwriters put junior capital at risk first, ahead of senior liquidity providers, keeping losses contained at the facility level rather than socialised across the pool.

The bigger opportunity goes beyond payment providers. Market makers could finance inventory without selling core holdings. Treasury teams could deploy idle digital assets into underwritten facilities with clear terms. Lenders could build structured credit products on shared infrastructure instead of building custom systems from scratch each time.

The unique angle here is that tokenization made assets portable. This protocol is trying to make them productive, which is the part of capital markets that has been missing onchain until now.

Related: XRP Whale-Retail Spread Hits 50.9% as Binance Gap Falls Amid Rising ETF Demand

Disclaimer: The information presented in this article is for informational and educational purposes only. The article does not constitute financial advice or advice of any kind. Coin Edition is not responsible for any losses incurred as a result of the utilization of content, products, or services mentioned. Readers are advised to exercise caution before taking any action related to the company.

, and Why Does It Matter in Crypto?")